Your hospital’s moat is not in Epic.

Healthcare’s next strategic advantage gets built in the layer above the EHR. The argument behind every Digital Scientists engagement.

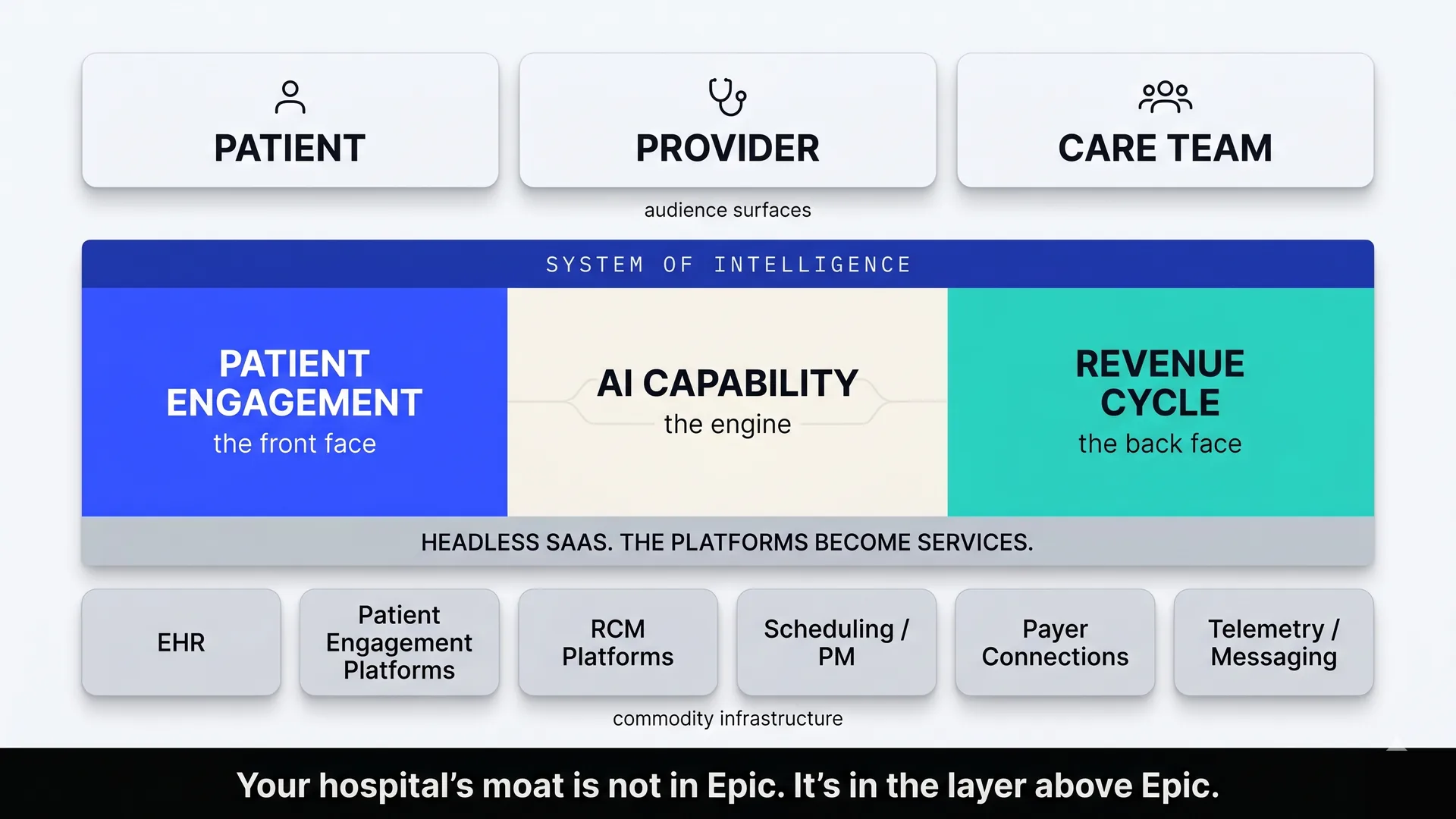

The system of intelligence sits above the EHR. The vendor platforms become commodity infrastructure beneath it.

The system of intelligence is where enterprise value is now migrating.

For two decades, enterprise software has been organized around the system of record. The platform that owned the database earned the rent. Salesforce won customer relationship management because it owned the customer database. Workday won human capital management because it owned the employee database. Epic won healthcare because it owned the patient record. Once an organization’s operating data lived inside one of these platforms, switching costs grew until they were prohibitive, and every third-party tool became a tenant paying rent to the system that owned the data.

That structure is being reorganized in real time. Capable AI agents have opened a new layer above the system of record: a reasoning and orchestration layer that reads across many systems at once, synthesizes context, decides what matters, and increasingly takes action. The industry has begun calling it the system of intelligence.

The framing is not new. Greylock’s Jerry Chen defined Systems of Intelligence in 2017 as the next defensible moat layer above systems of record and systems of engagement, and updated the argument in 2023. What’s new is that the consensus has hardened. Andreessen Horowitz published “From System of Record to System of Intelligence” in May 2026, defining the new layer as “the reasoning layer that sits above the database, and that increasingly treats the database as infrastructure.” Sequoia partner Konstantine Buhler has been making the same argument from the agent-economy lens since AI Ascent 2025.

In the new structure, the database is infrastructure. The system of intelligence is the institution’s primary asset.

“The reasoning layer that sits above the database, and that increasingly treats the database as infrastructure.” Andreessen Horowitz, May 14, 2026

In healthcare, the system of intelligence lives at the engagement-revenue boundary.

Healthcare’s systems of record are well known. Epic, Oracle Health, MEDITECH. The patient engagement platforms (Phreesia, Luma, Artera). The revenue cycle platforms (Waystar, Availity, R1). The eligibility services, the population health tools, the practice management systems. These platforms are entrenched, and they will remain so. They are not going to be replaced.

What healthcare does not yet have is the system of intelligence that sits above them. The layer that reads across the EHR, the portal, the RCM stack, the call center, the scheduling system, the population health platform. The layer that orchestrates context, decides what matters in a given moment, writes back into the appropriate system, and increasingly takes action in the world.

In practice, this layer sends the message to the patient who is missing a follow-up. It drafts the documentation prompt for the clinician about to undercode an encounter. It routes the 3am family call to the right nurse. It identifies the claim about to be denied for a fixable reason. It surfaces the population health gap and assigns the action.

Geographically, the healthcare system of intelligence lives at the engagement-revenue boundary. Patient Engagement is the front face. It is the orchestration that determines whether the right patient gets the right contact at the right time, in a form they can use, before small problems become bigger ones. Revenue Cycle is the back face. It is the orchestration that determines whether the right work gets captured for the right payer, with the right documentation, and denials prevented rather than chased downstream. AI capability is the engine that makes the integration practical now.

The two are inseparable. McKinsey’s January 2026 analysis “Agentic AI: The race to a touchless revenue cycle” projects that AI enablement of healthcare revenue cycle could cut cost to collect by 30 to 60 percent. For a 6 billion dollar health system, where revenue cycle costs typically run 2 to 3 percent of revenue, the same analysis projects 60 to 120 million dollars in annual savings. The financial gravity of the back face is now visible to every CFO.

But the back face only works when it reads from the front face. Documentation that supports clean claims comes from clinical workflow. Denial prevention rules come from payer plan rules. Both depend on reading across the same set of underlying systems and writing back into them. This is what the system of intelligence does. It is what the existing vendor stack cannot do on its own.

Patient engagement is the front face of your system of intelligence. Revenue cycle is the back face. They are two halves of one strategic asset.

The institution will own the integration layer. The vendors become infrastructure.

A reasonable question follows. Which vendor will own healthcare’s system of intelligence?

Epic will try. Its App Orchard already gestures at the role. The patient engagement platforms will try, extending upward from the portal. The revenue cycle platforms will try, extending upstream from the bill. Each one will attempt to do for healthcare what the go-to-market AI startups are doing for sales.

None of them will succeed in owning it outright. The system of intelligence has to read and write across systems that compete commercially. A patient engagement platform cannot orchestrate revenue cycle work without entering territory the RCM vendor will not concede. An RCM platform cannot orchestrate patient engagement at the journey level without entering territory the EHR will not concede. The EHR can do more than either, but no EHR will integrate openly with its competitors, and most health systems run more than one EHR somewhere in their footprint.

PitchBook’s April 2026 institutional research analyst note “AI Will Deliver Care to Billions and Break the System That Built It” makes the case from a venture-investor lens. Their first proprietary thesis: “Fragmentation of the delivery system, combined with the irreducibly personal nature of healthcare, will produce multiple winning care delivery models, not the winner-take-all dynamic typical of Big Tech platforms.” Their fourth thesis: “Last-mile execution is the key differentiator for success. The companies that solve the final connection between AI capability and patient outcome will capture disproportionate value.”

Andreessen Horowitz framed the same consequence differently: “gravity will come from orchestration.” In healthcare, gravity will come from the institution that builds the orchestration layer for itself.

The implication is structural. The system of intelligence in healthcare will be built at the institutional level, not bought from a single vendor. The hospital will own the integration layer that ties the rest together. The vendor platforms will become commodity infrastructure beneath it.

For this to work, the underlying SaaS platforms have to become functionally headless. Headless commerce and headless content management already transformed retail and publishing. The MACH Alliance has documented the pattern for enterprise architecture more broadly: open (transparent APIs, observable services, portable data, no dependency on a single vendor’s roadmap), composable (capabilities you can assemble, replace, and evolve independently), connected (designed to be optimized in an ecosystem rather than in isolation). The same shift is now overdue in healthcare. The platforms that accept it gracefully will earn an extended role as durable infrastructure. The platforms that resist will be progressively bypassed.

“Last-mile execution is the key differentiator. The companies that solve the final connection between AI capability and patient outcome will capture disproportionate value.” PitchBook Institutional Research, April 23, 2026

The technology stack is a commodity. The institution’s system of intelligence is not.

Every comparable hospital runs the same EHR. Every comparable hospital has the same vendor-supplied modules, the same patient engagement platform candidates, the same revenue cycle software pool. The technology stack is, increasingly, a commodity.

What is not a commodity is the system of intelligence the institution builds on top of it. That layer encodes everything specific to this hospital: how it actually delivers care, how its payer relationships actually work, how its providers actually document, how its patients actually behave, how its escalation paths actually run. It accumulates institutional knowledge no vendor can extract and no competitor can replicate. It is the one piece of a hospital’s technology stack that is genuinely its own.

In the language of the Andreessen Horowitz piece, “institutional memory becomes something a company can actually ship.” For a hospital, that institutional memory is the most valuable strategic asset on the balance sheet.

Hospitals that build a strong system of intelligence early will compound. Care quality improves because the intelligence layer acts on richer context. Financial performance improves because documentation is captured upstream and denials are prevented rather than chased. Patient satisfaction rises because the institution acts on what it knows. Staff burnout falls because the right work is routed to the right people. Each gain feeds the next.

Hospitals that delay will keep buying point solutions, wondering why none of them stick, and watching the AI-era advantage migrate to the institutions that figured out where it actually lived.

The Bain and KLAS Research 2025 healthcare AI study of 228 provider and payer executives makes the point in numbers. 70 percent of providers and 80 percent of payers now have an AI strategy in place or in development. Providers’ top investment priorities are revenue cycle management and clinical workflow. The strategies are forming. The investments are happening. The American Medical Association’s 2026 Physician Survey confirmed the same inflection from the clinician side: 81 percent of US physicians now use AI in practice, more than double the rate from 2023.

The question is no longer whether to build the system of intelligence. The question is whether the institution builds it, or rents it from someone else.

Your hospital’s moat is not in Epic. It is in the layer above Epic.

Digital Scientists operates two healthcare systems of intelligence today.

Most healthcare consultancies and most healthcare AI vendors write about the system of intelligence from outside. They publish frameworks, opportunity assessments, recommendation decks. Digital Scientists writes about it from inside. We operate two of them today.

NeverAlone, the front face.

Built for CommuniCare Health Services, a 2 billion dollar post-acute care organization, NeverAlone is a 24/7 virtual care command center that ingests signals from distributed care sites, triages incidents, dispatches care team responses, and tracks outcomes against operational SLAs. The platform serves over 26,000 patients per day across 130 plus post-acute locations, with a 96 percent treat-in-place rate and a 3-minute average response time. It reduced hospital readmissions by 30 percent. It operates 24 hours a day, every day of the year, HIPAA-compliant from day one.

Where telehealth is on-demand video, NeverAlone is the layer above. It is what happens when MyChart is not open. It ingests context from many sources, applies clinical and operational domain knowledge, decides what matters, takes action, and learns the institution’s patterns at scale. What happens at 3am in 130 post-acute locations is operating reality, not a theoretical question. NeverAlone is a working healthcare system of intelligence at the engagement face.

MDS Optimization, the back face.

Built on PointClickCare and in production with CommuniCare across multiple states, the MDS Optimization platform aligns diagnosis between systems of record, applies AI to non-clinical diagnosis recommendation, and writes back into the documentation that drives PDPM reimbursement. Independent financial analysis estimated more than 10 million dollars in PDPM revenue and 2 million dollars in Quality Incentives annualized from just two states. Documented healthcare impact across the full deployment exceeds 24 million dollars.

The platform works upstream of the bill, where documentation determines reimbursement before the claim is submitted. That is what the back face of an institutional system of intelligence is supposed to do. McKinsey’s 2025 RCM leaders survey found that 57 percent of leaders rank denial management and appeals as their top priority and 56 percent rank documentation and coding accuracy. 62 percent named denials and managing underpayments the top obstacle for 2026. Most RCM teams report spending 51 to 75 hours per week on denials-related work. The MDS Optimization approach removes that downstream burden by fixing the upstream work.

NeverAlone and MDS Optimization are both in production today. They are operating credentials, not slideware. They are also the proof that the system of intelligence is buildable now, by an institutional team, with the right engineering partner.

Most healthcare AI firms write about the system of intelligence from outside. Digital Scientists writes from inside. We operate two of them.

In May 2026, OpenAI and Anthropic paid roughly 15 billion dollars to back the same operating model.

This is an architectural decision, not a vendor decision. The CEO, COO, CMIO, value-based care architect, and integrated population health leader have already noticed that the engagement face and the revenue face are inseparable. The question is whether the institution builds the layer that ties them together, or keeps buying point solutions that paper over the gap.

In May 2026, the two largest AI companies in the world made the same bet, with billions of dollars of committed capital.

On May 4, Anthropic announced a joint venture with Blackstone, Hellman & Friedman, and Goldman Sachs to build “a new AI-native enterprise services firm that will work with companies to rapidly bring Claude into their core business operations.” The new firm is “a standalone entity with Anthropic engineering and partnership resources embedded directly within its team.” The consortium also includes General Atlantic, Leonard Green, Apollo Global Management, GIC, and Sequoia Capital. Healthcare is named explicitly as a target sector. Reported committed capital is approximately 1.5 billion dollars.

On May 11, OpenAI launched the OpenAI Deployment Company, majority-owned and controlled by OpenAI, with more than 4 billion dollars of initial investment (reportedly valued at 14 billion dollars by partner firms). The 19-firm consortium is led by TPG, with Advent, Bain Capital, and Brookfield as co-lead founding partners, and includes B Capital, BBVA, Emergence Capital, Goanna, Goldman Sachs, SoftBank, Warburg Pincus, and WCAS, plus consulting integrators Bain & Company, Capgemini, and McKinsey. The venture’s stated purpose, in OpenAI’s own words, is to “embed engineers specialized in frontier AI deployment, known as Forward Deployed Engineers, or FDEs, into organizations working on complex problems in demanding environments.” To accelerate from day one, OpenAI simultaneously acquired Tomoro, inheriting approximately 150 Forward Deployed Engineers and Deployment Specialists.

Both companies adopted the operating model Palantir invented and documented: embed senior engineers inside the customer’s operational environment, build production-ready workflows on the company’s stack, stay accountable until the system runs in production. Palantir CEO Alexander Karp made the architectural argument explicit in his February 2025 book The Technological Republic, an instant New York Times number-one bestseller.

The Forward Deployed Engineer model is not new. What is new is that the two most well-capitalized AI companies in the world just paid billions of dollars to validate it as the right way to deploy frontier AI into the enterprise.

The operating model is settled. The remaining question is who deploys it on behalf of the institution, and on what commercial terms.

In May 2026, OpenAI and Anthropic paid roughly 15 billion dollars to validate the operating model Digital Scientists has been running in healthcare since 2007.

Forward Deployed AI Engineering. Build, Operate, Transfer. The institution keeps what gets built.

Digital Scientists has been operating this pattern in healthcare since 2007. Forward Deployed AI Engineering is the named service. Senior product, design, and engineering pods embed close to the operation. They map the workflow, deploy the relevant capability, build the integrations, run governance and measurement, and stay accountable until the system earns its place in production.

Build, Operate, Transfer is the commercial structure. The institution receives the trained-on-its-data instance, the configurations, and the integration code as permanent assets. The platform Digital Scientists deploys becomes the layer the institution owns. Where the labs are structured to keep the platform and license access in perpetuity, Digital Scientists is structured to transfer the system of intelligence to the institution that paid to build it. The hospital ends up owning the AI capability trained specifically on its own data, payer relationships, clinical workflows, and patient population.

Model-agnostic.

Claude, GPT, Gemini, open-source. Whatever fits the institution’s security posture, performance requirements, and economics. No vendor lock-in by construction.

Healthcare-deep.

Real production proof in post-acute care, value-based care, revenue cycle, ambient clinical documentation, and patient and caregiver communication. Engineering grounded in the specific constraints of fragmented systems, PHI, and HIPAA compliance.

Your IP stays yours.

Digital Scientists does not route customer field feedback into a product roadmap. What we build for you does not become a feature in our next platform release. The institution’s data, the trained model weights, and the integration configuration transfer with the engagement.

The time to build is now.

The portal is a window into your data. The system of intelligence is the layer that knows what to do with it. Hospitals that build and own that layer will out-deliver every competitor running the same vendor stack. Hospitals that delay will keep wondering why none of the point solutions stuck.

External citations referenced in this essay

- Jerry Chen, “The New (New) Moats” (Greylock, 2017 / 2023)

- Ahern, Zhang, Immerman, “From System of Record to System of Intelligence” (Andreessen Horowitz, May 14, 2026)

- Sequoia Capital, AI Ascent 2025 keynote (May 2, 2025)

- McKinsey, “Agentic AI: The race to a touchless revenue cycle” (January 2026)

- McKinsey, “Healthcare RCM at a strategic turning point: Survey insights” (2025)

- MACH Alliance Principles (current)

- Bain & Company / KLAS Research, Healthcare AI Investment Study (October 9, 2025)

- PitchBook Institutional Research, “AI Will Deliver Care to Billions and Break the System That Built It” (April 23, 2026)

- Anthropic + Blackstone + Hellman & Friedman + Goldman Sachs JV press release (May 4, 2026)

- OpenAI Deployment Company announcement (May 11, 2026)

- Everest Group, “Palantir: Inside the Category of One” (Forward Deployed Engineering)

- Karp & Zamiska, The Technological Republic (Penguin Random House, February 2025)